When DeFi Stops Being DeFi

Permissioned tokens, RWAs, and the boundary where the cyber premise meets the law

Part 1 built the vault as DeFi's cornerstone; Part 2 walked the three challenges that arise when the asset behaves differently. All of that stayed inside DeFi's founding premise: permissionless, trustless, censorship-resistant — anyone can hold, anyone can transact, no one can freeze you. This post is about the axis where that premise doesn't just bend, it breaks. Real-world assets carry the law of a jurisdiction, and law has to be enforced. Permissioned tokens are where DeFi rails meet TradFi rules — and standing on that bridge, you are in neither world purely.

0. A different kind of axis

Parts 1 and 2 varied the shape of the claim — what it's worth (pricePerShare), when you can redeem it (sync vs ERC-7540 async), how its payoff resolves (ERC-1155 conditional tokens). Every one of those questions lives inside the permissionless model. You never had to ask who was allowed to hold the token, because the answer was always anyone.

Permissioning is a perpendicular question: not what the claim is, but who is legally allowed to hold or move it. It doesn't replace any standard from Parts 1–2 — it layers on top of them. And it's the one axis that puts you outside the cypherpunk premise entirely, because the reason it exists is external to the chain.

1. The collision: the physical world has laws

DeFi's origin story is adversarial to gatekeepers. A vault share, a stablecoin, an LP token — they're bearer instruments: hold the key, hold the asset, move it to anyone, and no issuer can stop you. That's the whole point. "Code is law" means the contract's logic is the only rule, and the contract doesn't care who you are.

A real-world asset does not get to make that choice. A tokenized US Treasury bill, a corporate bond, a real-estate share — the underlying exists inside a jurisdiction, and that jurisdiction comes with securities law, KYC/AML, sanctions screening, tax reporting, and courts. You cannot tokenize a regulated security and wish those away; the legal reality travels with the asset onto the chain.

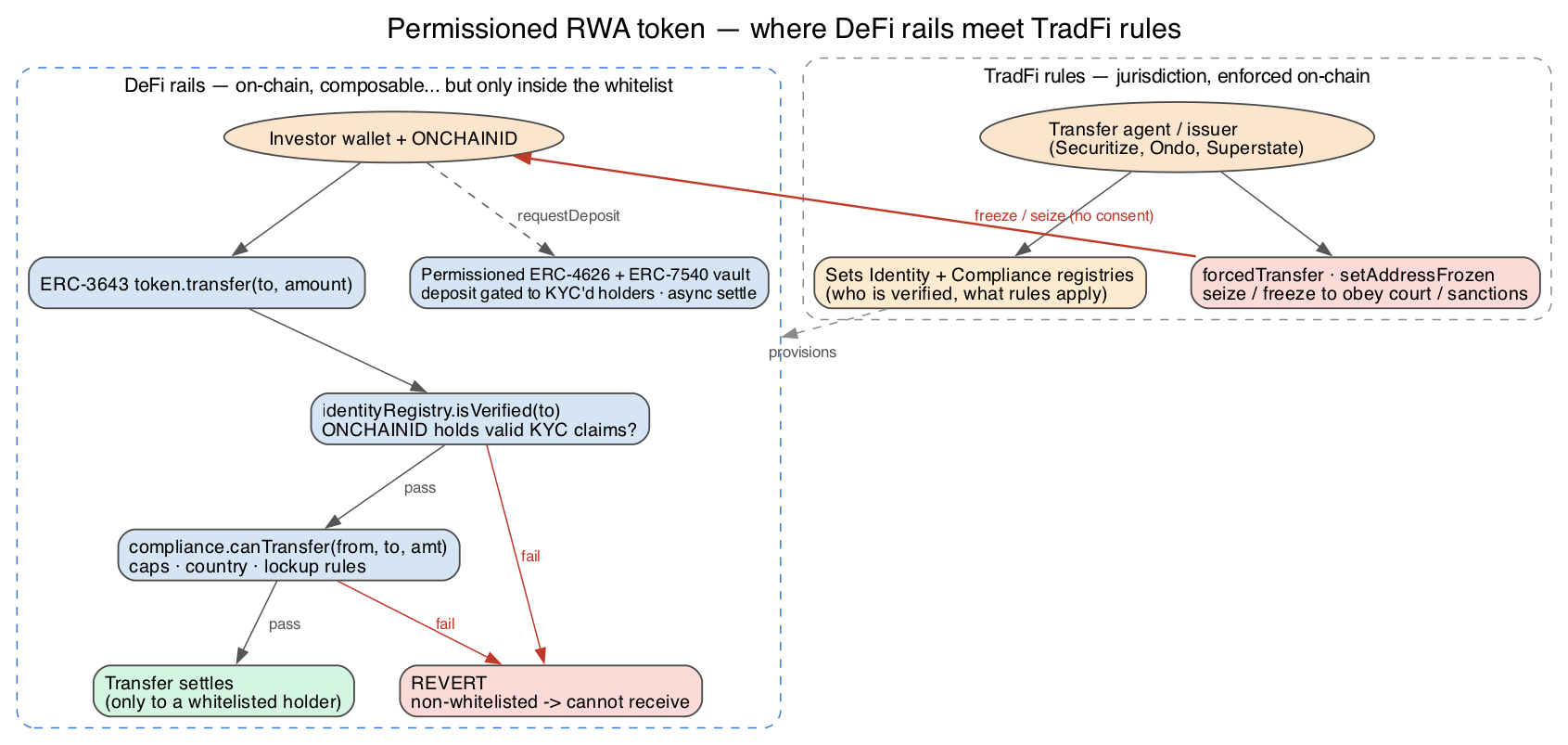

And here's the crux: those laws have to be enforceable. A regulator or a court doesn't accept "the smart contract is immutable, sorry." If a holder is sanctioned, their tokens must be freezable. If a court orders restitution, the tokens must be moveable without the holder's key. Off-chain paperwork can't enforce that on a bearer token that anyone can move in one block — so the enforcement has to be pushed into the token itself.

That is the collision. Code-is-law meets law-is-law, and law-is-law wins — because the asset's value depends on the legal system recognizing it. The moment you accept that, you've left permissionless DeFi.

2. Importing enforcement into the token

To satisfy the law, a permissioned token has to do three things a normal ERC-20 never does:

- Gate who can hold it — an on-chain identity / allowlist. Only verified (KYC'd, accredited, non-sanctioned) wallets may receive tokens. A transfer to a non-whitelisted address simply reverts.

- Gate how it moves — programmable compliance: holding-period lockups, per-country caps, max-holder counts, qualified-purchaser rules.

canTransfer(from, to, amount)must return true before any transfer settles. - Override the holder — and this is the sharpest break. A designated transfer agent / issuer can freeze a balance or force-transfer it to another address without the holder's consent, to obey a court order, a sanctions list, or a recovery request.

That third power is the clean inversion of everything DeFi promised. Censorship-resistance means no one can freeze or seize your assets. A permissioned RWA token ships with a function whose entire job is to let someone do exactly that. It's not a bug or a backdoor — it's a legal requirement, deliberately built in. But it means the token is only as trustless as the entity holding the controller key.

3. The standards that encode it

Three standards (one dominant, two older cousins) express this on-chain.

ERC-3643 (T-REX) — the dominant one

ERC-3643 reached Final status in December 2023 — the first compliance-token standard to do so — and is maintained by Tokeny and the nonprofit ERC-3643 Association. It's a suite of six on-chain components working together:

| Component | Role |

|---|---|

| Token | The ERC-20-style asset, but every transfer is gated. |

| Identity Registry | The whitelist of verified investors. |

| Identity Registry Storage | Shared storage of verified identities. |

| Compliance | The rule engine (caps, country limits, lockups). |

| Trusted Issuers Registry | Who is allowed to attest to an investor's claims. |

| Claim Topics Registry | Which claims (KYC, accreditation…) a holder must carry. |

A transfer only settles if both gates pass:

// ERC-3643, the two checks that live inside every transfer.

function transfer(address to, uint256 amount) public override returns (bool) {

// 1) Is the recipient a verified investor? (their ONCHAINID must hold valid

// claims from trusted issuers on the required topics)

require(identityRegistry.isVerified(to), "recipient not verified");

// 2) Do the programmable compliance rules allow this specific transfer?

require(compliance.canTransfer(msg.sender, to, amount), "compliance blocked");

_transfer(msg.sender, to, amount);

compliance.transferred(msg.sender, to, amount);

return true;

}

// The TradFi override — enforcement powers a normal ERC-20 never has:

function forcedTransfer(address from, address to, uint256 amount) external onlyAgent;

function setAddressFrozen(address holder, bool frozen) external onlyAgent;

function freezePartialTokens(address holder, uint256 amount) external onlyAgent;

Identity is carried by ONCHAINID — a per-investor identity contract holding signed claims (KYC, accreditation) issued by trusted parties. The wallet isn't the identity; it's linked to one.

ERC-1400 and ERC-1404 — the family

- ERC-1400 (Polymath, ~2018) is an umbrella of sub-standards: ERC-1594 (core transfers with reason codes), ERC-1410 (partially-fungible balances split into named partitions — e.g. locked vs unlocked, or share classes), ERC-1643 (documents), and ERC-1644 (controller operations:

controllerTransfer/controllerRedeem— the same force-transfer power). It never reached Final and is losing new issuance to ERC-3643. - ERC-1404 is the minimalist take: a tiny ERC-20 extension exposing

detectTransferRestriction(from, to, value) → uint8(0 = allowed) and a human-readablemessageForTransferRestriction(code). Also never officially finalized, but dead simple and ERC-20-compatible.

4. Where this meets Parts 1–2: permissioned vaults

This is the loop back to the vault. A permissioned ERC-4626 vault is a normal vault whose mutating entrypoints are gated: deposit/mint (and share transfer) require an allowlisted caller — often implemented by having maxDeposit/maxMint return 0 for non-approved addresses so the standard interface still behaves. Morpho's curated/permissioned vaults are a production example of allowlist-gated markets.

For RWAs specifically, permissioning almost always fuses with the ERC-7540 async pattern from Part 2 — and now you can see why the two travel together:

- Permissioning handles who (KYC gate before you can deposit at all).

- ERC-7540 handles when (the underlying T-bill settles T+N off-chain, and compliance/subscription windows can't resolve synchronously, so

requestDeposit/requestRedeemqueue the action for later fulfilment).

An institutional RWA vault is therefore often "ERC-4626 accounting + ERC-7540 async settlement + an ERC-3643-style permission layer" — every standard from this series stacked into one contract.

5. In the wild

The tokenized-treasury market is the clearest live example. As of early 2026 the pattern is identical across the leaders: allowlisted / KYC'd holders, plus an issuer or transfer agent that can freeze and force-transfer.

| Product | Issuer / agent | Model |

|---|---|---|

| BUIDL | BlackRock, tokenized by Securitize (SEC transfer agent) | Permissioned ERC-20; qualified purchasers only; transfers to non-whitelisted wallets revert; multi-chain. The largest tokenized-treasury fund (multi-billion). |

| Ondo OUSG | Ondo Finance | Permissioned ERC-20, KYC + qualified-purchaser, backed largely by BUIDL. |

| Ondo USDY | Ondo Finance | Aimed at non-US retail; permissionless secondary transfers after an initial lockup; issuer retains freeze. |

| Superstate USTB | Superstate (manager Invesco as of Mar 2026) | Allowlist-enforced — both parties to a transfer must be approved. |

(AUM figures move quickly and vary by source — check rwa.xyz for current numbers before quoting any.)

Every one of them, without exception, keeps the freeze-and-seize powers. That's not a coincidence — it's the price of admission for holding a real-world security on-chain.

6. The honest reckoning

So is this DeFi? Yes and no — and the "no" is the interesting half.

What you gain: access to real, regulated yield (Treasuries, credit) with on-chain settlement, transferability within a whitelist, 24/7 operation, and programmable composition with the rest of your on-chain stack. Institutional capital can finally touch the rails.

What you surrender:

- Permissionlessness — you must be approved before you can hold anything.

- Composability — a transfer-restricted share reverts on transfer to any non-whitelisted address, so it cannot flow through generic AMMs, lending markets, or unpermissioned vaults. Composability survives only inside the walled garden of whitelisted venues. The money-lego snaps only onto other approved legos.

- Censorship-resistance — a controller key can freeze or move your balance without your consent. Necessary for legal recovery and sanctions; fatal to the original promise.

| Permissionless DeFi (Parts 1–2) | Permissioned RWA (Part 3) | |

|---|---|---|

| Who can hold | Anyone with a wallet | Allowlisted / KYC'd only |

| Transfer to a stranger | Always works | Reverts unless they're verified |

| Can you be frozen? | No — code is law | Yes — setAddressFrozen, forcedTransfer |

| Composability | Full — any protocol | Only within whitelisted venues |

| Why the rule exists | Chosen (cypherpunk premise) | Imposed (jurisdiction & courts) |

| Governing logic | Code is law | Law is law |

The takeaway for the whole series: Part 1 asked what makes the share worth more. Part 2 asked when it settles and how its payoff resolves. Part 3 asks a question the first two never had to — will the protocol even let you hold it, and can someone take it back? That question doesn't have an on-chain answer. It has a legal one. Permissioned tokens are the exact point where DeFi stops being purely DeFi and starts being a bridge: DeFi rails, TradFi rules. Cross it knowing which side each promise comes from.